The Partnership sends updates for the most important economic indicators each month. If you would like to opt-in to receive these updates, please click here.

Estimated Reading Time: 2 minutes.

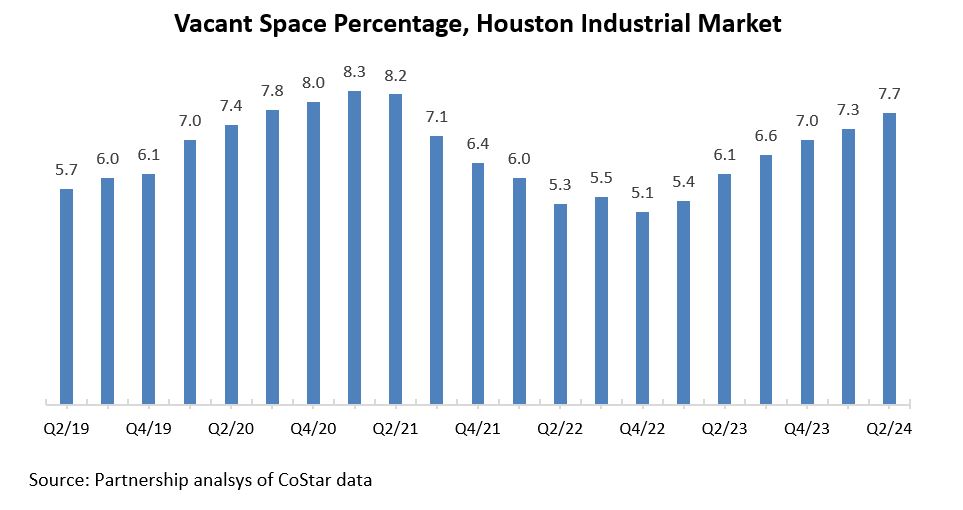

The demand for industrial/warehouse space in Houston continues to decline. In Q4/22, the vacancy rate was at a low of 5.1 percent but has since increased to 7.7 percent in Q2/24.

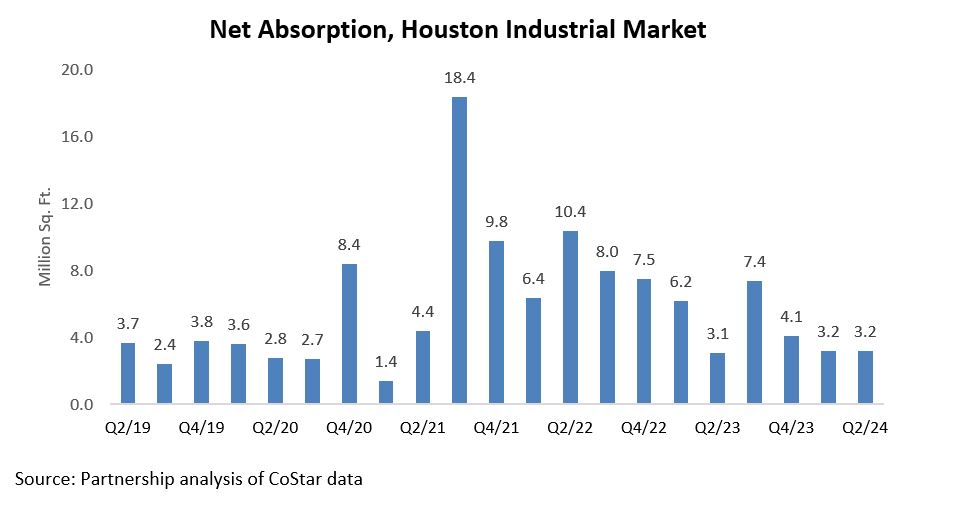

Demand for space peaked at 18.4 million square feet in Q3/21. In Q2/24, absorption stood at 3.2 million square feet, reminiscent of pre-pandemic levels.

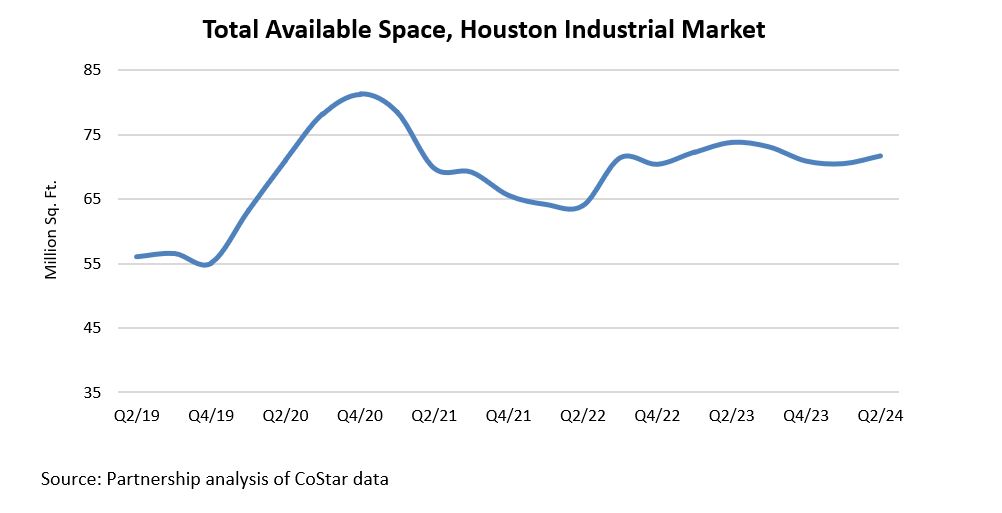

Houston had 71.7 million square feet of industrial/warehouse space (direct and sublet) available at the end of Q2/24. This includes vacant, occupied yet available, available for sublease, or available at a future date.

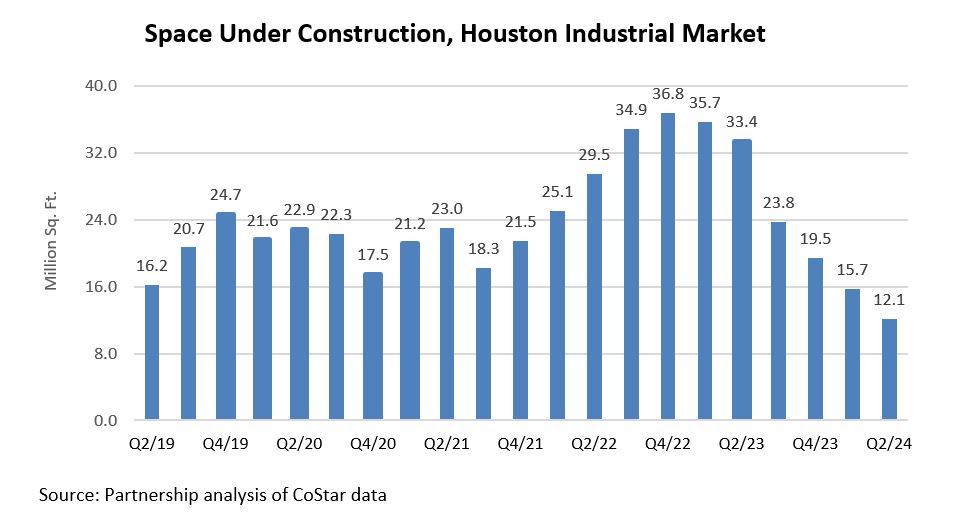

Higher interest rates, tougher lending standards, and weaker net absorption have hampered building activity. As of Q2/24, Houston had 12.1 million square feet underway compared to 36.8 million at the Q4/22 peak.

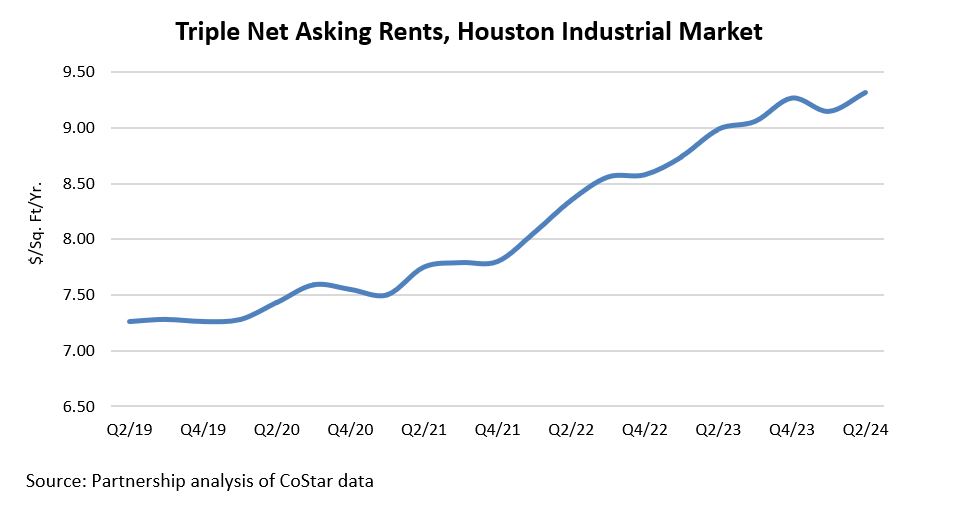

Rents continue to rise, however. The average industrial rent was $9.32/sq. ft./year in Q2/24. That’s up from $8.99 in Q2/23 and $8.35 in Q2/22. The rates quoted are triple net (NNN) where the tenant is responsible for all expenses associated with their share of building occupancy, i.e., taxes, maintenance, utilities, security, etc. Despite the record amount of new supply delivered in ‘23, Houston continues to see a rise in rents year over year, climbing 3.7%.

Prepared by Greater Houston Partnership Research

Leta Wauson

Research Director

lwauson@houston.org

Patrick Jankowski, CERP

Chief Economist

Senior Vice President, Research

pjankowski@houston.org

Houston industrial vacancy rate ticked up to 7.7% as of Q2 24.

Stay up-to-date on what’s happening with the Partnership and Greater Houston region by opting-in to receive information on upcoming events, news, data releases and more.