The Partnership sends updates for the most important economic indicators each month. If you would like to opt-in to receive these updates, please click here.

Estimated Read Time: 1 minute

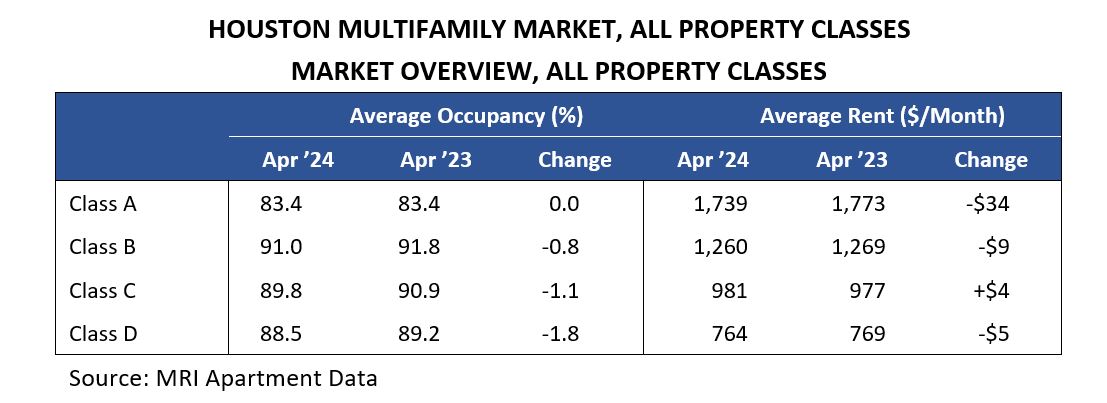

Multifamily in Houston has shifted from a landlord-friendly to a tenant-friendly market. Average occupancy has fallen below 90 percent or is headed in that direction for all property classes. Rents have not seen the typical upswing that occurs in the spring. Incentives and discounts are common. And developers continue to overbuild.

The Houston market absorbed roughly 17,300 Class A apartment units in the 12 months ending April ’24, according to Partnership analysis of MRI Apartment Data. Normally, that would be a strong performance. However, Class A inventory expanded by nearly 21,000 units over the same period. The Partnership estimates there are almost 31,000 unoccupied Class A units in the market, up from 29,600 units this time last year. At current rates of absorption, that’s almost a two-year supply.

The mismatch between supply and demand has impacted rents. The typical Class A unit rents for $1,739. That’s down $34 (1.9 percent) from May of last year. Rents for Class A units in lease-up, i.e., properties opened 13 months, is $1,615, down from $1,716 in May of last year.

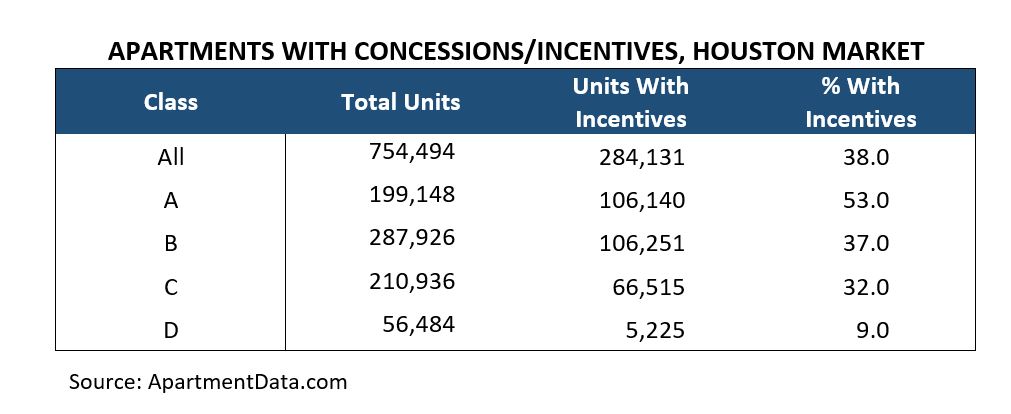

The decline in occupancy has spurred owners to offer concessions to draw prospective tenants to their properties. This may include free rent, waiver of a security deposit, or floorplan upgrades. As of May ’24, over half of all Class A units have an incentive, over one-third for B, and just under one-third for Class C. The concessions have effectively reduced monthly rents by 5.0 to 7.0 percent.

About 20,000 apartment units, virtually all Class A, were under construction as of May 1. Another 32,760 were proposed or in the planning stages. An industry rule of thumb holds that Houston absorbs one apartment unit for every six jobs created. At the current pace of construction, Houston will need to create roughly 120,000 jobs to absorb what’s currently under construction.

Prepared by Greater Houston Partnership Research Department

Patrick Jankowski, CERP

Chief Economist

Senior Vice President, Research

pjankowski@houston.org

Leta Wauson

Research Director

713-844-3661

lwauson@houston.org

The occupancy rate for Class A units in April '24

View data on the cost of living in Houston compared with other major U.S. metros.

Review the latest data on this key economic indicator.

Review the latest information on home sales in the Houston region.

Stay up-to-date on what’s happening with the Partnership and Greater Houston region by opting-in to receive information on upcoming events, news, data releases and more.